The BVR has published its quarterly digest and we thought you’d find the following points interesting.

We look to the US as well as the UK when thinking about valuation statistics, as the US still leads the world. BVR is a very good free source of information if you are interested too. You can see its latest quarterly digest here.

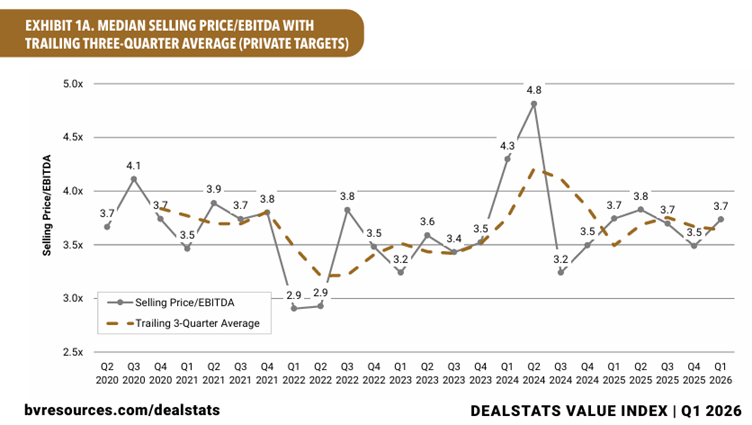

For those of you who do not have time to read the whole report, here are some useful graphs offering insights into the multiples being paid for private companies.

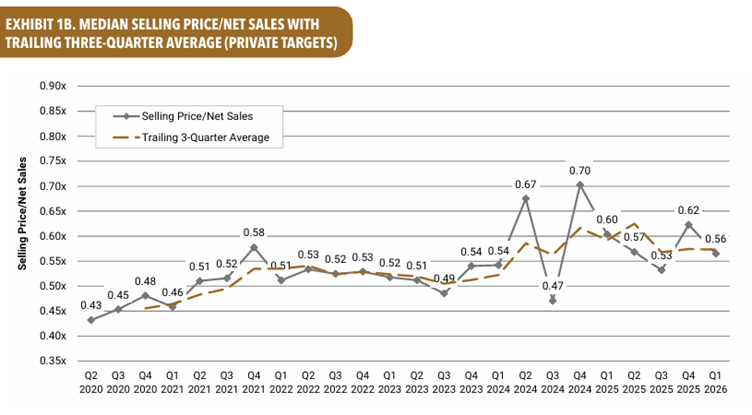

As these stats are based on a selling price, they are very useful as a general guide to establish a willing-buyer-willing-seller, open market, arm’s length price.

As you can see from this chart and the one above, median multiples for private companies, whether revenue or EBITDA, tend to be more cautious than the headline numbers you read about in relation to the high risk VC-backed companies that pull it off!

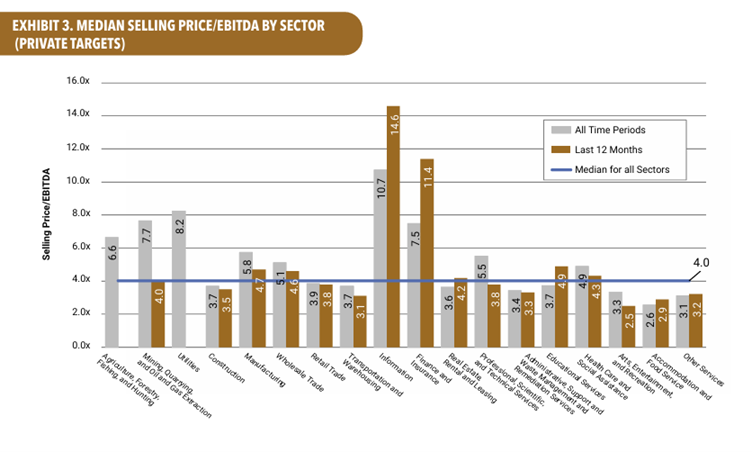

Here, you can see that very few sectors command high exit multiples and for many the MEDIAN EBITDA multiples are well below 4x.

Of course the devil is in the detail, especially in the Information sector where all those AI companies will be lurking! You can also see that asset rich and high yielding sectors tend to command higher multiples.

It is interesting to see that Finance and Insurance is also a bit of an outlier. This is probably because of the high margin nature of many activities in that sector.

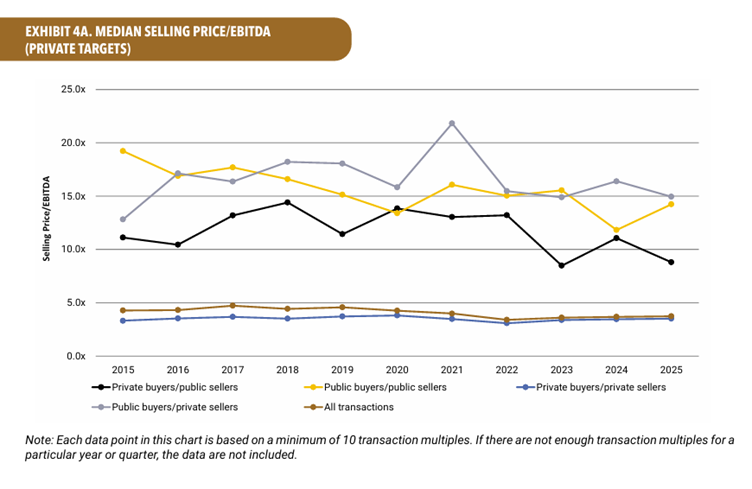

Lastly, this chart is interesting in what it tells you about private vs public market transactions.

There are two clear messages. Public markets transact at much higher multiples than private to private transactions and the volume of private to private transactions is such that it pulls median selling price/EBITDA for all transactions back to the level for private to private transactions.

What does this mean for you and Athla?

It is going to be in our interests to seek out public market clients, as transactions should command higher values and of themselves be more interesting and valuable to work on. Meanwhile, we all need to push forward hard with helping private companies buy from, or sell to, other private companies because this is where the volume work will sit.

Overall, it is interesting that despite macro-economic and global political challenges and the rest, the story around EBIDTA and Revenue multiples does not really shift much year-to-year in the private markets, but in the public markets the volatility means that timing a transaction can make all the difference between it being quite expensive or remarkably cheap!

We specialise in valuations of private companies, shares, assets (contracts anyone?) and IP – both registered and unregistered – as well as other intangibles like creative rights. Do you have something on your desk, especially complex matters, which requires an expert valuer to unpick the threads and produce a strong defensible report which all parties can rely on? If so, please give us a buzz or email us.

![]()